Fully Indexed Rate on ARM What is it?

Fully Indexed Rate – What is it?

When you get an Adjustable Rate Mortgage (ARM) you get an initial rate that is fixed for a certain period of time say five years for example. After the first five years of the loan, your interest will begin to adjust based on two factors: your index and your margin. The mortgage interest rate that your mortgage loan will adjust to after the fixed period is called the Fully Indexed Rate.

Fully Indexed Rate is the combination of the index the mortgage lender has chosen plus the fixed margin the mortgage lender places on the mortgage loan. This is often different than the initial rate offered, or the start rate. The fully indexed rate will only fluctuate at the adjustment period of your ARM, and may be subject to caps that determine how much they may increase within a certain time period.

Mortgage Rate (Fully Indexed Rate) = Index + Margin

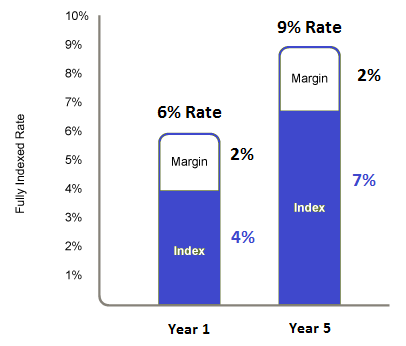

Note: In the picture above the margin remains the same but the index changes which will change the Fully Indexed Rate at each adjustment period.

Fully Indexed Rate Example

For example, lets assume you got a 30 year mortgage loan that was a 6.0% 5 year ARM. What this means is that you have a mortgage loan for the next 30 years and the mortgage interest rate for the first 5 years is fixed at 6.0%. After the first five years, your mortgage interest rate will then change based on two factors: index and margin. The index is picked when you get the mortgage loan and will always be that same index. For this example we will use a LIBOR Index. The margin is determined by the mortgage lender at the time you get the ARM Loan and is also fixed for the life of the loan. Your mortgage interest rate (Fully Indexed Rate) at the adjustment period is determined by adding the current index rate to the margin to come up with your current mortgage interest rate. So if you have a fixed margin of 2.0% then you would add 2.0% to whatever the index was at the time of adjustment. So if the LIBOR index was 3.0% then the interest rate would be 2 + 3 = 5.0%. Your new interest would drop from 6.0% to 5.0% in this example.

Apply for Adjustable Rate Mortgage

If you have more questions on Adjustable Rate Mortgages or would like to apply for a mortgage loan, please feel free to call me at 302-703-0727. You can also APPLY ONLINE.

John R. Thomas – NMLS 38783

Certified Mortgage Planner – Primary Residential Mortgage, Inc.

302-703-0727 DE Office / 610-906-3109 PA Office / 410-412-3319 MD Office

248 E Chestnut Hill Rd, Newark, DE 19713

#AdjustableRateMortgages

#FullyIndexedRate

#DelawareMortgageLoans

#DelawareMortgages

#JohnThomasTeam

#DelawareAdjustableRateMortgages