VA Loan Limits 2026: Key Facts Veterans and Active Duty Service Members Should Know

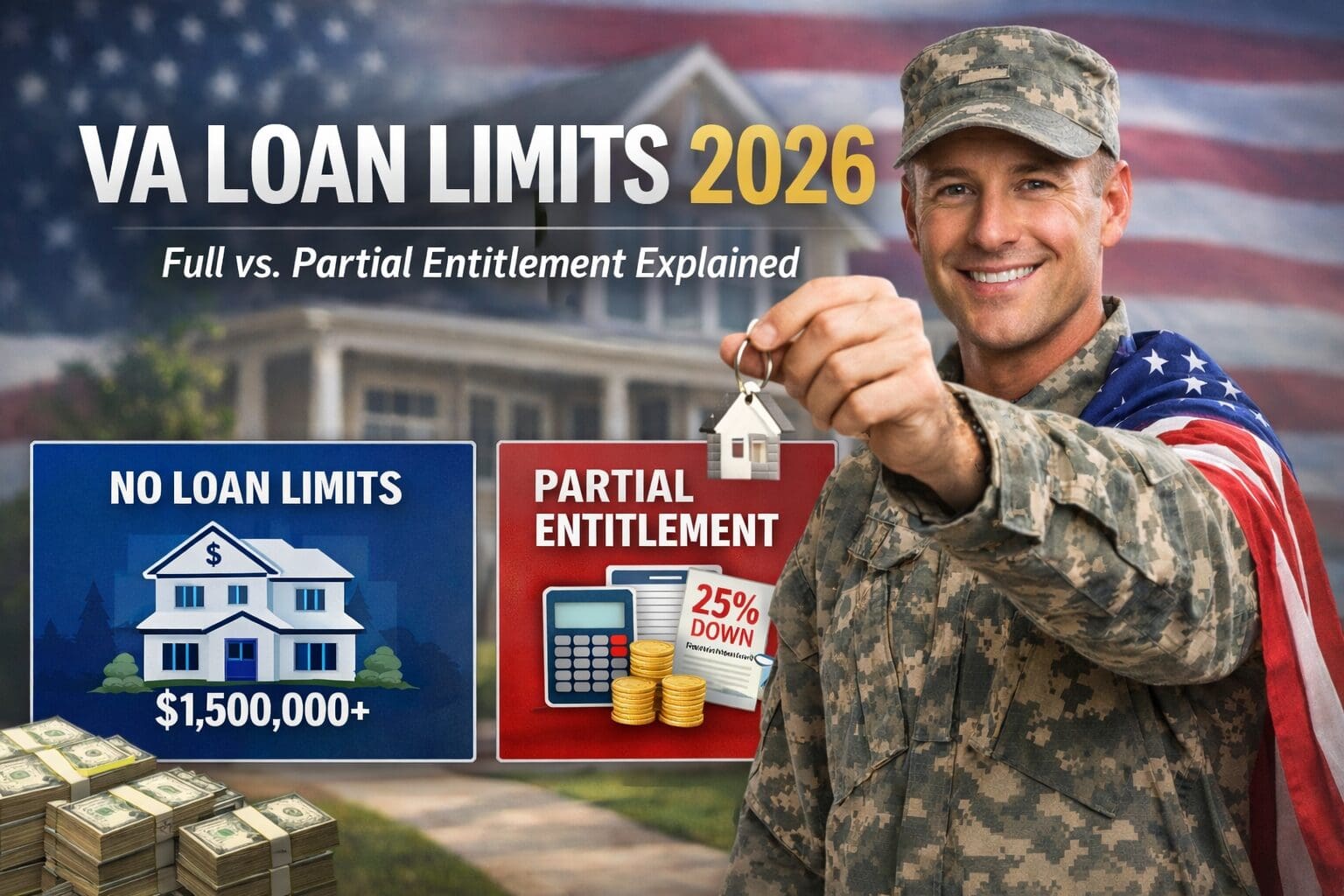

VA loan limits for 2026 will only apply to veterans with partial entitlement. Veterans and active-duty service members who have full VA entitlement (100%) will have no loan limits. They can borrow up to 100% of the home’s purchase price even if it exceeds $1,500,000. If the vet has partial VA entitlement, the FHFA’s 2026 conforming loan limits come into play, and borrowing above your remaining entitlement loan limit will require a 25% down payment on the difference. Need to get pre-approved for a VA Home Loan to purchase or refinance, then call Loan Office John Thomas at 302-703-0727 or APPLY ONLINE.

What are the VA Loan Limits for 2026?

People often misunderstand VA loan limits. With the Blue Water Navy Vietnam Veterans Act, the VA stopped setting loan limits if veterans have their full entitlement.

Here’s the easy rule:

- 100% entitlement ? No loan limit with VA loans

- Partial entitlement ? Loan limits still apply

VA Loan Limits in 2026 (With Partial Entitlement)

If a veteran has partial entitlement, VA lenders need to use the FHFA conforming loan limits for 2026.

- Max Base Loan Limit: $832,750

- Max High-Cost Area Loan Limit: $1,249,125

The Federal Housing Finance Agency (FHFA) sets these limits every year. These limits apply if your entitlement is not fully restored to 100%.

Full VA Entitlement: No Limits on Loan Amount

When you have your full entitlement, you can finance 100% of the entire purchase price, no matter how much the home costs.

Example:

- Purchase price: $1,500,000

- VA entitlement: 100%

- Down payment required: $0

- VA base loan amount: $1,500,000

There is no cap as long as income, credit, and appraisal support the loan.

Partial VA Entitlement: How the Math Works

When entitlement is partial, the lender must calculate remaining entitlement. That determines how much you can borrow with 0% down.

Example with Partial Entitlement

- Maximum 100% financing allowed: $500,000

- Purchase price: $550,000

- Difference: $50,000

- Required down payment: 25% of $50,000 = $12,500

Final numbers:

- Down payment: $12,500

- VA base loan amount: $537,500

This calculation is exact and required by VA guidelines.

VA Funding Fees for 2026

The VA funding fee is added to all VA loans unless the Veteran is exempt and helps keep the program available with no monthly mortgage insurance.

Who Is Exempt?

Veterans with VA disability compensation are exempt. If exempt, the total loan amount equals the base loan amount. The Veteran’s Certificate of Eligibility (COE) will determine if Veteran is Exempt or Not Exempt from paying the VA Funding Fee.

How the VA Funding Fee Is Calculated

The funding fee depends on:

- Exempt vs. non-exempt

- First-time vs. subsequent use

- Down payment amount

The funding fee can be financed into the loan.

VA Funding Fee Examples (2026)

First-Time Use – 0% Down

- Base loan: $500,000

- Funding fee: 2.15%

- Fee amount: $10,750

- Total loan amount: $510,750

Subsequent Use – 0% Down

- Base loan: $500,000

- Funding fee: 3.30%

- Fee amount: $16,500

- Total loan amount: $516,500

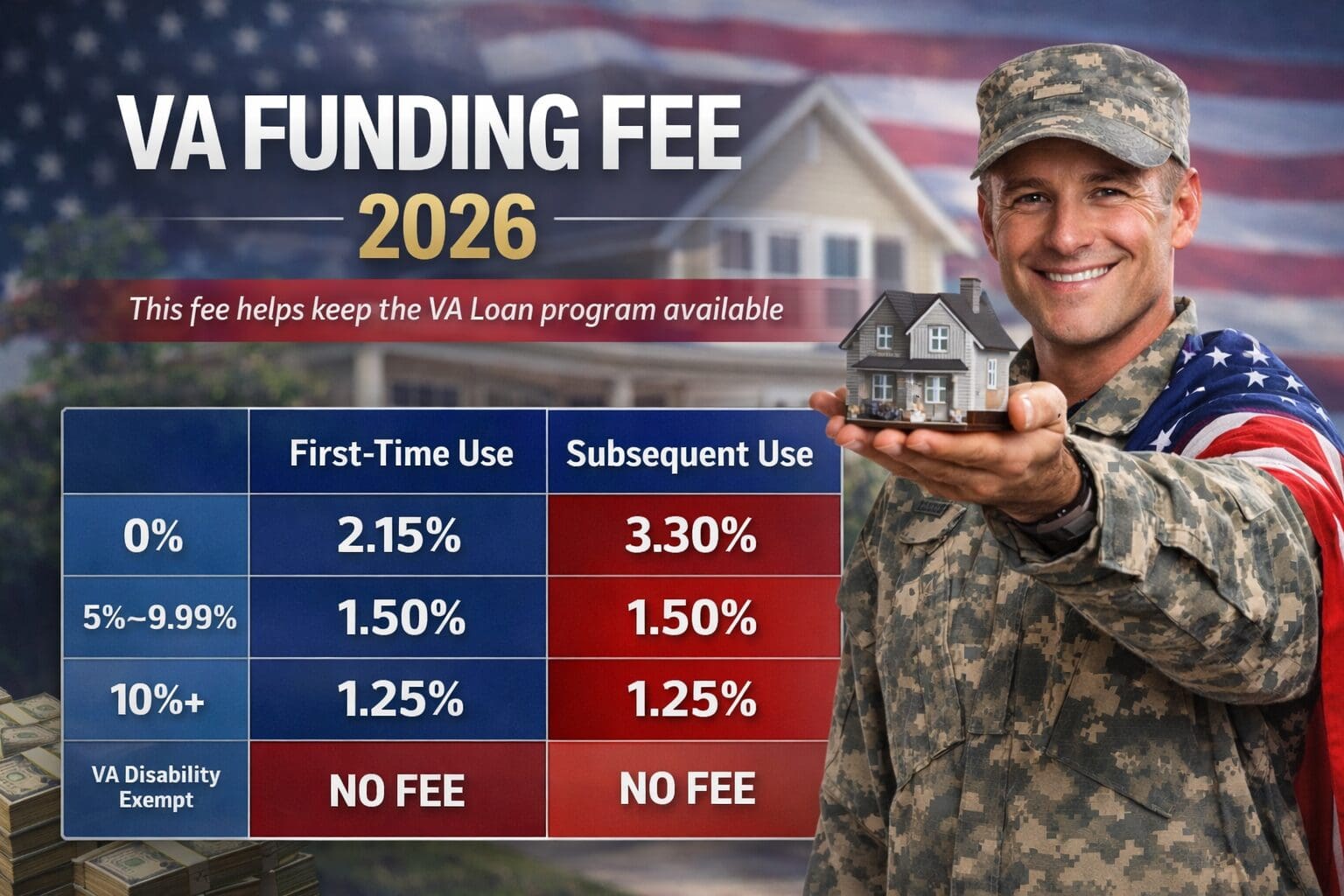

VA Funding Fee Table (2026)

| Down Payment | First-Time Use | Subsequent Use |

|---|---|---|

| 0% | 2.15% | 3.30% |

| 5%–9.99% | 1.50% | 1.50% |

| 10%+ | 1.25% | 1.25% |

| VA Disability Exempt | 0% | 0% |

What VA Home Loan Options Does a Vet Have in 2026?

Veterans and active duty service members have several different options for using their VA home loan benefit in 2026 to purchase a home. The following is a list of the available VA Home Loan Options for Veterans:

The following are the available VA Home Loan options for refinancing a home with a VA Loan:

Clearing Up VA Loan Limit Myths

- Myth: VA loans have a limit of $832,750

- Fact: This applies when using partial entitlement

- Myth: Jumbo VA loans need down payments

- Fact: Full entitlement removes the need for any down payment

- Myth: All veterans must pay funding fees

- Fact: Veterans with a VA disability don’t pay anything

How John Thomas Supports Veterans with VA Loan Limits

VA loans demand precise work on entitlement, funding fees, and lender know-how. VA Loan Expert John Thomas helps by:

- Obtaining COE to determine VA entitlement

- Calculating any required down payments based on VA entitlement

- Ensuring funding fees are applied correctly

- Explaining details clearly before you make an offer

No confusion. No last-minute issues. Find out how much you qualify for by contacting Loan Officer John Thomas at 302-703-0727 or APPLY ONLINE

Common Questions on VA Loans

Will there be VA loan limits in 2026?

Yes, but if you have partial entitlement. There are no limits when you have full entitlement.

What does full VA entitlement mean?

It means you can use your full VA benefit without any loan limit.

Is it possible to borrow over $1 million using a VA loan?

Yes, if you have full entitlement and meet the income requirements.

Do county differences affect VA loan limits?

They matter when you have partial entitlement especially in high-cost regions.

Do I always have to pay the VA funding fee?

No, if you qualify for a VA disability exemption, you won’t need to pay it. Your Certificate of Eligibility (COE) will determine if you are exempt or Not Exempt from the VA Funding Fee.

Can I include the VA funding fee in my loan?

Yes, it’s possible to roll the VA funding fee into your total loan amount. Most Veterans opt to finance the VA funding fee.

Want to Check Out Your VA Entitlement?

If you are on active duty or a veteran and need to learn how much you can borrow in 2026, your next move is to get a VA entitlement review.

Book a consultation with John Thomas to:

- Help Obtaining your VA Certificate of Eligibility (COE)

- Verify whether you have full or partial entitlement

- Get pre-approved for a VA Home Loan & Find out your exact borrowing limit

- Get your VA loan set up right from the beginning

Straightforward answers. Precise calculations. Guidance made for veterans. Call John Thomas today at 302-703-0727 or APPLY ONLINE