DSCR Loans | Investor Cash Flow & Rental Property Guide

DSCR Loans: A Complete Guide for Real Estate Investors

A DSCR loan (Debt Service Coverage Ratio loan) allows real estate investors to qualify for a mortgage based on the rental income of the property rather than personal income. Lenders calculate DSCR by dividing gross rental income by the proposed mortgage payment, including principal, interest, taxes, insurance, and association dues. These loans are commonly used for long-term rentals, short-term rentals, and portfolio expansion, and are considered a type of Non-QM investor financing.

Are you a Real Estate investor who is hoping to maximize your earning potential but don’t want the hassle of having to document your income in order to get an Investor Mortgage Loan? Then we’re excited to present you with the DSCR Investor Cash Flow Loan Program for the purchase or refinance of an investment property without having to document your income to qualify. We will qualify you off the cash flow of the property you are buying or refinancing. Call 302-703-0727 to get started today or you can APPLY ONLINE.

What is a DSCR Loan?

A DSCR loan, or Debt Service Coverage Ratio loan, is a mortgage designed for real estate investors. Instead of qualifying based on tax returns or employment income, the lender evaluates whether the property’s rental income can cover the proposed mortgage payment. This makes DSCR loans especially useful for:

• Investors with multiple properties

• Self-employed borrowers

• Investors who write off significant expenses

• Portfolio builders scaling quickly

DSCR loans are considered Non-QM (Non-Qualified Mortgage) loans because they do not follow traditional agency income documentation rules.

The Investor Cash Flow Mortgage Loan or DSCR Loan allows a real estate investor to use the cash flow on the subject property to be used to qualify for the new mortgage loan. The program covers loans for non-owner occupied properties between one and four units as well as 5-20 units and even Mixed-Use Properties. No tax returns or employment information is required to qualify for the loan. There is no limit to the number of financed properties. This innovative program can be used effectively to build a portfolio of income generating rental properties.

How is the DSCR Calculated?

The debt service coverage ratio (DSCR) of the subject property is used to calculate the ratio that can be used to qualify as follows:

- DSCR is defined as gross rents divided by qualifying PITI & HOA. 100% of the rents can be used for DSCR calculation.

- DSCR is greater than 1 then the property is cash-flowing (The gross rent greater than the mortgage payment including principal, interest, taxes, insurance, and any property association fees then you have a cash flowing property)

- DSCR can be equal to 1 or less than 1 which means no or negative cash flow – If Negative cash flow then will need 12 months of reserves for the negative cash flow.

The formula is simple:

Gross Monthly Rent ÷ Monthly PITIA = DSCR Ratio

PITIA includes:

• Principal

• Interest

• Taxes

• Insurance

• HOA dues (if applicable)

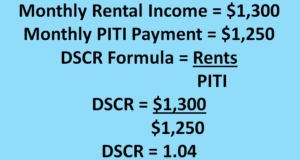

Example:

Monthly Rent: $2,500

Monthly PITIA: $2,000

$2,500 ÷ $2,000 = 1.25 DSCR

A 1.25 ratio means the property generates 25% more income than the mortgage payment.

DSCR Sample Calculation:

What is a Good DSCR Ratio?

A “good” DSCR ratio is really defined by the investor and his/her investment goals. There are essentially three different scenarios for DSCR ratios based on the cash flow of the property:

- 1.00 = Break-even

- Above 1.00 = Positive cash flow

- Below 1.00 = Negative cash flow

We have DSCR loans programs for each of these scenarios:

- 1.00 DSCR = minimum standard for basic DSCR Loan

- Below 1.00 allowed with additional reserves

- No Ratio DSCR (no rental income calculation required)

Who Qualifies for a DSCR Loan?

Qualifying for a DSCR Loan is not the same as qualifying for a traditional conventional loan, it is much easier more streamlined. Below are the qualification guidelines:

- Minimum 600 Credit Score to apply

- Loans up to $5.0 million (minimum loan $75,000)

- Up to 85% LTV on purchase of 1-4 unit properties

- No Personal Income Provided (No tax returns or Pay Stubs)

- No DTI Restrictions as qualify on DSCR Ratio

- No Employment required

- Can Close in Name of LLC or Business Entity

- Up to 75% LTV on 2-8 Units Mixed Use Properties

- Up to 75% LTV on 5-10 Units Residential Properties

- 40 Year Term with Interest-only available

- Seller Paid Closing Costs are allowed up to 6%

- Can be Used for Purchase, Cash-out or Rate/Term Refinance

- 100% Gift Funds permitted

- First Time Investors are eligible

- Vacant Properties are eligible

- Short Term Rentals are allowed (AirDNA Reports Accepted)

What Type of Properties are Eligible for This Loan?

The DSCR Investor Cash Flow loan can be used to finance a variety of different types of properties. The Following is a list of the eligible property types:

- Single Family Rental Homes

- Townhouses

- 2 – 4 unit residential properties

- Multi Units up to 25 units

- Mixed-Use Properties (2-10 Units)

- PUDs

- Warrantable Condos

- Non-warrantable Condos

- Condotels

DSCR for Short Term-Rentals

There are specialized DSCR Loans for purchasing or refinancing short term rental income properties using:

- 12-month rental history

- AirDNA reports

- Market rent analysis

DSCR Loans for ITIN Borrowers

We offer DSCR Loans for borrowers using an ITIN instead of a Social Security Number

Learn more about ITIN DSCR Loans

DSCR vs Conventional Investment Loans

Conventional investment loans:

- Require full income documentation

- Limit number of financed properties (no more than 10 financed properties)

- Count debt-to-income ratio (DTI)

- Have Loan Level Price Adjustments (LLPAs) that make the rates much higher

- Require Mortgage Insurance (MI) above 80% LTV

- Cannot Close in LLC, Must close in personal name

DSCR loans:

- Focus on property cash flow

- No DTI calculation

- No limit on number of finance properties

- No MI above 80% LTV

- No LLPAs

- Can Close in name of LLC

What are the Requirements for Closing in the Name of an LLC?

In order to close an Investor Cash Flow Loan in the name of an LLC, you must meet the following guidelines:

- LLC must have been formed only for the purchase or management of real estate.

- For Multi member LLCs with varying membership interest , a fully executed Board Resolution authorizing the borrower to enter the loan contract.

- Borrowers must personally guarantee the loan

What Documents are needed from the LLC?

- Operating Agreement to include authorization to borrower & designates signers.

- Certificate of Formation / Articles of Organization

- Certificate of Good Standing or equivalent document

- Certificate of Foreign Qualification of other qualification to operate in the state where business is being conducted (if entity is formed in a state other than where business is being performed)

- Name and Principal residence / home address that will be signing the Personal Guaranty if multiple members with greater than 20% interest

What about Pre-Payment Penalty?

DSCR Loans are not required to have a pre-payment penalty BUT you will get a better interest rate if you take a pre-payment penalty. The pre-payment penalty options are as follows:

- No Pre-Payment Penalty

- 1 year Pre-Payment Penalty

- 2 Year Pre-Payment Penalty

- 3 Year Pre-Payment Penlaty

- 4 Year Pre-Payment Penalty

- 5 Year Pre-Payment Panalty

Deciding on whether to have a pre-payment penalty or not and which one to choose, depends on your investment goals and the current interest market. If rates are low compared to the last 3-5 years then taking a longer pre-payment penalty to get the lowest rate possible would make sense but if interest rates are near a 3-5 year high then no or 1-2 year pre-payment penalty would make sense.

If you choose to get a pre-payment penalty to get better rate, make sure the time line fits with when you might sell the property.

What are the credit requirements for a DSCR Loan?

Your credit score will determine your maximum loan to value which impacts your required down payment. You can do as little as 15% down but must have a minimum 680 credit score. Below is list of minimum credit scores by loan to value (LTV)

85% LTV – Minimum Score 680

80% LTV – Minimum Score 660

75% LTV – Minimum Score 640

70% LTV – Minimum Score 620

60% LTV – Minimum Score 600

Pros and Cons of DSCR Loans

Advantages

• No personal income documentation

• Scalable for portfolio growth

• Entity ownership allowed

• Flexible underwriting

Considerations

• Higher rates without pre-payment penalty

• Prepayment penalties common

• Reserve requirements may be higher

Ready to Expand Your Investment Portfolio?

If you are evaluating DSCR financing for a rental property, the first step is reviewing the property’s projected cash flow and your liquidity position.

Schedule a consultation with Loan Officer John Thomas to discuss:

• Target property analysis

• DSCR ratio review

• Loan-to-value options

• Prepayment strategy

• Entity structuring considerations

Clear planning leads to stronger portfolio decisions.

How Do You Apply for an DSCR Loan?

If you are interested in getting more information or would like to apply for an Investor Cash Flow Mortgage Loan, You can APPLY ONLINE HERE, or you can call Loan Officer and DSCR Loan Expert John Thomas at 302-703-0727.

John R. Thomas – NMLS 38783

Certified Mortgage Planner – Primary Residential Mortgage, Inc.

302-703-0727 DE Office / 610-906-3109 PA Office / 410-412-3319 MD Office

248 E Chestnut Hill Rd, Newark, DE 19713

Frequently Asked Questions About DSCR Loans

What credit score is required for a DSCR loan?

Credit score requirements vary by the loan-to-value. Many DSCR programs begin at 600, with stronger pricing available for higher credit scores.

How much down payment is required for a DSCR loan?

DSCR loans require as little as 15% down, but lower credit scores require higher down payments.

Can I use an LLC to purchase with a DSCR loan?

Yes. DSCR lenders allow entity ownership, with the borrower providing a personal guarantee on the loan.

Are short-term rentals eligible for DSCR financing?

There are DSCR Loans for short-term rental income qualification using rental history or third-party market data.

What happens if the property’s DSCR is below 1.00?

Lenders allow lower ratios with additional reserves to make up for the negative cash flow or alternative program options such as No Ratio DSCR Loans

Do DSCR loans require tax returns?

No. DSCR loans qualify based on rental income from the subject property rather than personal tax returns.

Are there limits to how many properties I can finance?

DSCR programs do not limit the number of financed properties but lenders will usually limit have many loans they will have for one individual themselves.

Do DSCR loans include prepayment penalties?

Pre-Payment Penalties are NOT required but do allow for better interest rates so they are a personal decision.