VA Home Loans Explained: How Veterans Buy Homes With $0 Down

VA Home Loans Explained: How Veterans Buy Homes With $0 Down

For Veterans, active duty service members, and eligible military spouses, VA home loans are one of the most powerful home financing programs available today. Many military families are surprised to learn they may be able to buy a home with zero down payment, no monthly mortgage insurance, and competitive interest rates.

As a VA Loan Officer and VA Home Loan expert, John Thomas helps Veterans understand how to use their Veteran Loan benefits to achieve homeownership while avoiding common mistakes that can delay approvals or increase costs.

If you are researching VA Loans, looking for a trusted VA Lender, or trying to understand how VA Home Loans work, this guide will walk you through everything you need to know. Questions? Call Loan Officer & VA Home Loan Expert John Thomas at 302-703-0727 or APPLY ONLINE.

Watch the Full VA Home Loan Explanation Video

What Are VA Home Loans?

VA Home Loans are mortgage programs backed by the Department of Veterans Affairs. These Veteran Loans were created to help military families purchase homes with flexible qualification guidelines and reduced financial barriers.

A VA Lender, such as the John Thomas Team with Primary Residential Mortgage, provides the mortgage financing, while the Department of Veterans Affairs guarantees a portion of the loan. This guarantee reduces lender risk, allowing qualified borrowers to receive more favorable loan terms compared to many conventional mortgage options and FHA Loans.

VA Home Loans can be used to purchase single-family homes (SFR), townhomes, condominiums, manufactured homes, and 2-4 unit properties when the borrower occupies one of the units as their primary residence. Purchasing a multi-unit home with your VA Loan allows you to purchase an income producing property with $0 Down.

How Veterans Buy Homes With $0 Down Using VA Loans

One of the most recognized advantages of VA Home Loans is the ability for eligible borrowers to purchase homes without a down payment. Most mortgage programs require buyers to save thousands of dollars before purchasing a home. VA Loans allow qualified military borrowers to finance up to 100 percent of the purchase price.

While zero down payment does not always mean zero out-of-pocket costs, many closing expenses may be negotiated with the seller as seller paid closing costs or you can look to use the PRMI Military Down Payment Assistance Program for eligible Veterans. This allows Veterans to preserve savings while still becoming homeowners.

Why VA Loans Do Not Require Monthly Mortgage Insurance

Most low down payment mortgage programs require monthly mortgage insurance to protect the lender. This additional cost increases a borrower’s monthly payment. For example, Conventional Loans require Private Mortgage Insurance (PMI) and FHA and USDA require mortgage insurance monthly and an upfront Mortgage Insurance Premium or Upfront Guarantee Fee.

VA Home Loans do not require monthly mortgage insurance. Instead, the VA program includes a one-time VA funding fee that helps sustain the program. The funding fee can be financed into the loan balance rather than paid upfront and most veterans choice to finance the funding fee to save on cash out of pocket. Veterans receiving is disability are exempt from paying the VA funding Fee.

This benefit alone can save Veteran homebuyers hundreds of dollars per month compared to FHA or conventional financing with monthly mortgage insurance.

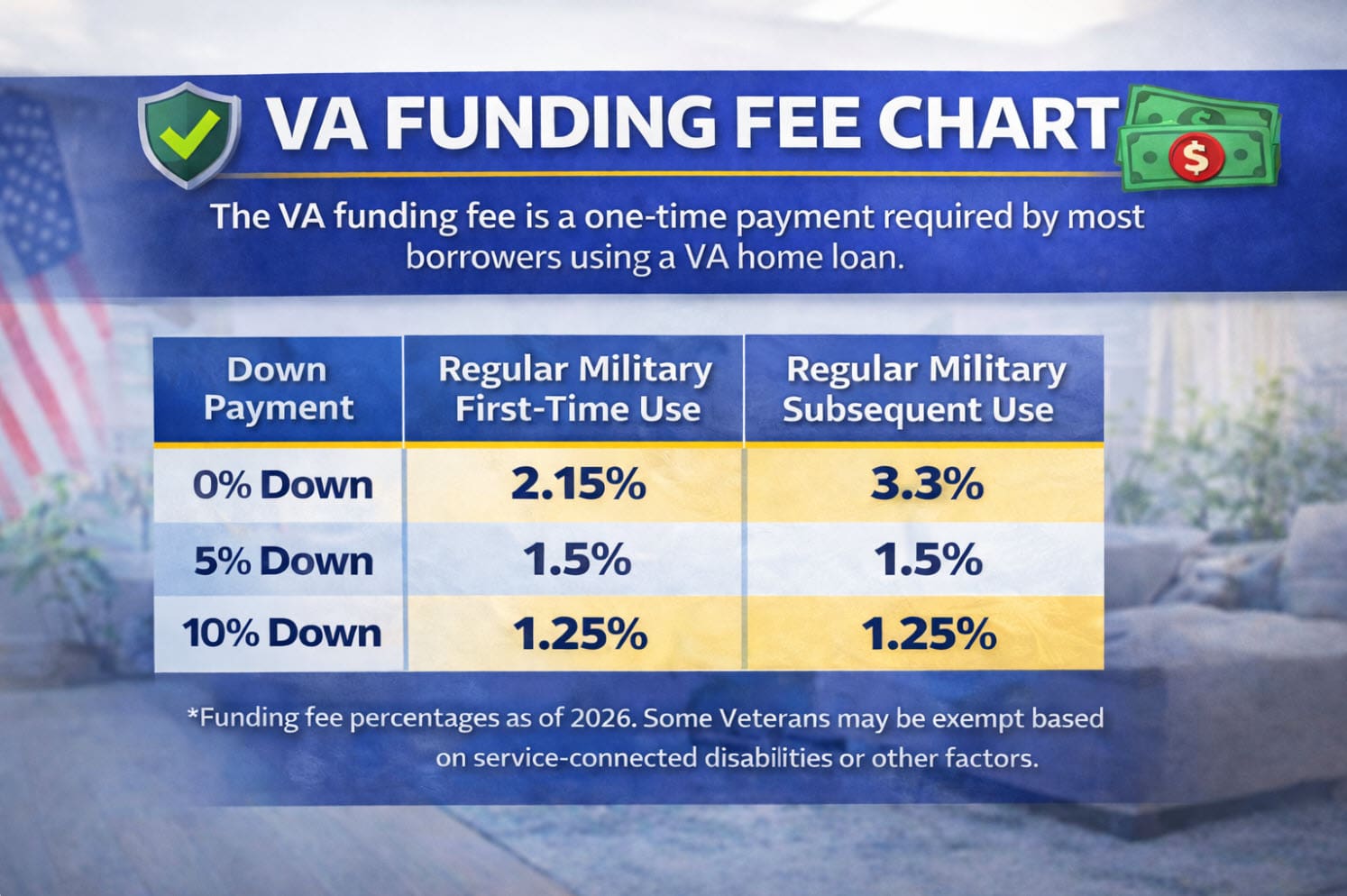

What is the VA Funding Fee?

The VA funding fee is charged by the Department of Veteran Affairs on VA Home Loans so that the VA can continue to provide VA lenders with guarantees to insure the lender for losses on VA Home loans that default for a portion of the loss. The VA funding fee is required on every VA Loan unless the veteran is exempt. Veterans with disability are exempt from paying the funding fee.

The funding fee is different depending on whether the it is a purchase or a refinance loan, whether it is first time use or subsequent use and whether you are putting down and down payment. Below is VA Funding Fee Chart:

What is the VA Residual Income Requirement?

VA residual income is a VA underwriting test that looks at what you have left over each month after paying your proposed housing payment (principal, interest, taxes, insurance, and any HOA) plus your recurring monthly debts. VA defines residual income as the net income remaining after those deductions—basically the “money left for family support” for normal living expenses like food, utilities, transportation, and savings. It’s one of the ways VA evaluates whether the payment is realistic, not just whether your debt-to-income ratio fits a box.

VA compares your residual income to guideline tables that vary by region, household size, and loan amount, and lenders calculate it on the VA loan analysis form. A key practical rule is that if your DTI is over 41%, VA generally expects closer review unless your residual income is strong—often defined as at least 20% above the guideline amount—so strong residual income can help support approvals that might look tight on DTI alone.

Who Qualifies for VA Home Loans?

VA Loan eligibility is primarily based on military service. Borrowers may qualify if they meet service requirements established by the Department of Veterans Affairs. Eligible borrowers include:

- Active duty military personnel

- Veterans

- National Guard members

- Military reservists

- Eligible surviving spouses

Eligibility is earned by serving in the Army, Air Force, Navy, Marines, Coast Guard, Space Force, National Guard and Reserves.

Eligibility is verified through a Certificate of Eligibility, commonly called a COE. A qualified VA Loan Officer or VA Lender can assist borrowers in obtaining this documentation. Having Trouble obtaining your COE? Give John Thomas a call at 302-703-0727 to get assistance.

Beyond military service eligibility, borrowers must also meet financial qualification standards. VA Lenders evaluate credit history, income stability, debt levels, and overall ability to repay the mortgage.

Why VA Loans Often Offer Competitive Interest Rates

Because VA Home Loans are partially guaranteed by the Department of Veterans Affairs, lenders assume less financial risk. This reduced risk often results in lower interest rates compared to traditional mortgage options such as Conventional Loans.

Lower interest rates directly reduce monthly payments and improve long-term affordability. This is one of the reasons VA Loans remain one of the most valuable home financing benefits available to Veterans.

VA Property and Occupancy Requirements

VA Loans are designed to help Veterans purchase primary residences. Borrowers must intend to live in the home as their main residence. VA Home Loans cannot be used to purchase investment-only properties or second homes.

Homes financed using VA Loans must also meet minimum property standards established by the Department of Veterans Affairs. These standards help ensure homes are safe, structurally sound, and suitable for occupancy. A VA appraiser will be be assigned by the VA once your lender orders the VA appraisal through the VA website. The VA appraiser will visit the property and inspect to make sure meets VA minimum property requirements (MPR). If there are any required repairs to meet minimum property standards then the VA appraiser will make the appraisal report subject to required repairs that must be completed prior to closing on the VA home loan.

There is an option to not make the required repairs by using a VA Renovation Loan. The VA renovation loan allows you to finance 100% of the purchase plus the required repairs and the repairs are completed after closing on the home.

Common VA Loan Misconceptions

Many buyers and real estate professionals misunderstand VA Loans. Some believe VA Home Loans are difficult to close or require perfect credit scores. In reality, VA Loans often provide flexible credit guidelines as VA has no minimum required credit score and can close efficiently when handled by an experienced VA Loan Officer.

Another common myth is that Veterans can only use their VA Loan benefit once. Veterans can use VA Home Loans multiple times throughout their lifetime depending on entitlement availability. There is not limit on the number of times a veteran can get a VA home loan. Veterans can also refinance their VA loan with either a VA IRRRL Streamline Refinance or a VA Cash-Out refinance.

A veteran can also get a new VA Home Loan without paying off a current Veteran loan. A veteran can turn their current home into an investment property and keep their current VA loan and also get a new VA Loan to purchase a new home. The lender will complete a remaining entitlement calculation to determine how much they can borrower for 100% financing on the new purchase. If the veteran wishes to purchase a home for more than this amount they will just be required to put down 25% of the difference as a down payment.

When VA Home Loans Make the Most Sense

VA Loans are often ideal for:

- First-time military homebuyers

- Veterans relocating through PCS orders

- Military families looking to minimize upfront costs

- Borrowers seeking competitive interest rates

- Veterans wanting to preserve savings

A knowledgeable VA Lender such as Loan Officer John Thomas can help determine whether a VA Loan is the best financing option based on each borrower’s financial goals and housing plans.

Step-by-Step VA Home Loan Process

Understanding the VA home buying process helps borrowers feel confident and prepared. The typical process includes:

- Verifying VA Loan eligibility by obtaining a COE

- Completing mortgage pre-approval for VA Home Loan

- Shopping for a home with a qualified real estate agent

- Contract acceptance and VA appraisal

- Underwriting review and final loan approval

- Closing on the home

Working with an experienced VA Loan Officer helps ensure each step is completed efficiently and accurately.

Why Choosing the Right VA Loan Officer Matters

VA Loans involve specialized guidelines that differ from other mortgage programs. Choosing a knowledgeable VA Loan Officer helps borrowers avoid delays, misunderstandings, and unnecessary costs.

John Thomas specializes in helping Veterans and military families understand their financing options while providing clear communication throughout the home buying process. His experience working with VA Home Loans allows borrowers to confidently navigate eligibility, underwriting, and closing requirements.

Work With a Trusted VA Lender and VA Loan Officer

If you are a Veteran or military service member considering buying a home, speaking with an experienced VA Loan Officer can help you understand your eligibility and financing options before you begin house hunting.

John Thomas provides personalized VA Loan consultations designed to help military borrowers:

- Understand eligibility and entitlement

- Review credit and income qualification

- Estimate buying power and payment options

- Navigate the VA home buying process step-by-step

Schedule Your Free VA Loan Consultation

Schedule your free VA loan consultation with John Thomas.

Schedule Your Free VA Loan Consultation

Call or Text John Thomas: 302-703-0727

Loan Officer: John Thomas

Primary Residential Mortgage, Inc.

NMLS 38783

Frequently Asked Questions About VA Home Loans

Do VA Loans really allow zero down payment?

Yes, eligible borrowers can finance 100 percent of the purchase price.

Are VA Loans only for first-time homebuyers?

No. Veterans can use VA Home Loans multiple times depending on entitlement availability.

Do VA Loans require mortgage insurance?

VA Loans do not require monthly mortgage insurance, which helps lower monthly payments.

Can active duty service members qualify for VA Loans?

Yes. Active duty personnel may qualify once minimum service requirements are met.

- VA Loans

- VA Home Loans

- VA Lender

- VA Loan Officer

- Veteran Loan

- VA Mortgage Program

- Military Home Loans

- VA Loan Eligibility

- VA Loan Benefits

- VA Loan Zero Down Payment

- VA Loan Requirements

- VA Loan Pre Approval

This article is for educational purposes only and is not a commitment to lend. Loan approval is subject to credit approval, underwriting guidelines, and VA program eligibility requirements. Terms and availability may change without notice.