VA One-Time Close Construction Loan: Build Your Home With One Loan | John Thomas, VA Construction Loan Expert

Last updated: November 2, 2025

VA One-Time Close Construction Loan (2025 Guide)

If you’ve earned VA loan benefits and want to build a custom home instead of buying an existing one, the VA One-Time Close Construction Loan makes it possible. Also known as a VA construction-to-permanent or single-close construction loan, this program lets eligible veterans, active-duty service members, and surviving spouses finance the land, construction, and permanent mortgage in one loan—with no down payment required.

I’m John Thomas (NMLS 38783), a mortgage loan officer specializing in VA and construction financing. My team helps veterans nationwide navigate the build-your-own-home process using this powerful VA benefit. Call me at 302-703-0727 to talk to a VA Lending Specialist about a VA Construction Loan or get started online at APPLY ONLINE

What is a VA One-Time Close Construction Loan?

A VA One-Time Close (OTC) Construction Loan combines three phases into one transaction:

- Land purchase or payoff (if you already own land)

- Construction financing, paid to your licensed builder in draws

- Conversion to a permanent VA mortgage after completion

You close once, qualify once, lock your rate up front, and move in when the home is complete—without re-qualifying or paying a second set of closing costs.

Key benefits of VA OTC Construction Loan:

Like most other VA home loans, VA one-time close construction loans require the borrower to occupy the home once it’s finished. The Veteran must also be the primary occupant of the home, with provisions being made for those who are called to active duty service, deployments and other types of military duty that requires the Veteran to be away

Another thing you must know, most VA loan transactions will require a VA loan funding fee. However, Veterans who are eligible to receive VA disability benefits may get the dual benefit of no down payment and no VA loan funding fee.

- Zero down payment: finance up to 100% of land + build costs + Closing Costs if supported by appraised value.

- Single closing: one set of documents for land, construction, and permanent mortgage

- Fixed-rate protection: lock your interest rate before construction begins with Float Down Option at End of Construction.

- No monthly mortgage insurance (PMI)

- Minimum 620 Credit Score but can go lower with compensating factors

- No DTI Limit, must meet VA Residual Income Requirement

- PRMI Will allow the use anywhere in the U.S. for a primary residence except New York

- No Mortgage Payments During Construction, Payments Begin when home is complete and Certificate of Occupancy (CO) issued.

- No Loan Limits for 100% financing with Full VA Entitlement.

- No Re-Qualification at the end of construction for the permanent VA Loan.

Who is eligible

- Eligible veteran, active-duty, National Guard/Reserve, or surviving spouse with a valid Certificate of Eligibility (COE)

- Primary residence only (1–4 units if you will occupy one unit)

- Credit score: 620 minimum score (Can go lower with compensating factors)

- Debt-to-income: up to 50% but can go higher if meet residual income requirements

- Builder must be licensed, insured, and experienced

- Property must meet VA Minimum Property Requirements (MPRs) upon completion

How the process works (step-by-step)

- Pre-approval & COE: verify VA eligibility and get pre-approved with a lender experienced in VA OTC construction.

- Select lot and builder: choose a licensed, insured contractor; finalize plans, specs, and budget. Build on owned land or purchase land at closing.

- Underwriting & appraisal: lender reviews the package; VA appraiser values the proposed construction.

- Single closing: close once on the combined land + construction + permanent loan. Funds go into a construction escrow.

- Construction & draws: lender releases funds in stages after inspections. Payments may be interest-only or deferred until completion depending on program.

- Final inspection & conversion: after certificate of occupancy, the loan converts to a standard VA mortgage without re-qualification.

Typical loan terms and requirements (2025)

| Feature | VA One-Time Close |

|---|---|

| Loan type | 30-year fixed rate |

| Down payment | 0% (up to 100% financing based on reasonable value) |

| Max LTV | Up to 100% of reasonable value |

| Minimum credit score | Typically 620 but can lower with compensating factors |

| Loan amount limits | No VA loan limit with full entitlement; appraisal and lender guidelines apply |

| Construction period | Commonly up to 12 months; extensions may be possible |

| Prepayment penalty | None |

| Property type | 1-unit primary residence; some lenders allow up to 4 units |

| Land | Purchase Land or Build on Land You Already Own |

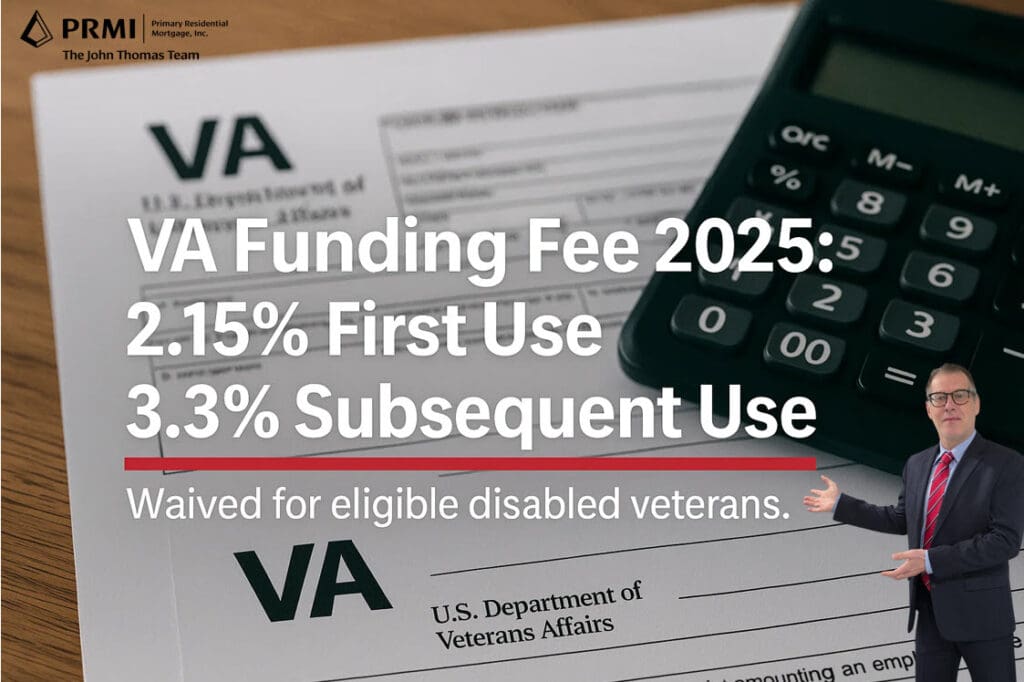

VA funding fee for construction loans

The standard VA Funding Fee applies to construction loans like purchase loans and can be financed into the loan amount.

- First-time use (0% down): 2.15%

- Subsequent use (0% down): 3.30%

- Exemptions: veterans with qualifying service-connected disabilities

There is no monthly mortgage insurance on VA loans.

Builder and property requirements

- Builder must be licensed, insured, and provide a one-year builder’s warranty

- Plans must comply with state/local codes and VA MPRs

- Permanent foundation and standard utilities required

- Manufactured/modular may be eligible if permanently affixed and meet HUD/VA standards

- Construction period must meet lender and program timelines

- VA No Longer Requires Builders to be registered with the VA

- No Self Build, Veteran cannot be their own builder.

Can You Build a 2-4 Unit Property with VA Construction Loan?

Yes, you can build a multi-unit property with a VA Construction Loan BUT the Veteran MUST occupy one of the units as their primary residence. There are extra requirements from the VA to qualify to build a 2-4 unit property listed below:

- Must have a 660+ Credit Score

- Cannot Solely Qualify from Future Rents on other units

- Must have 6 Months Reserves for VA Loan on 2-4 unit property

- If no previous rental experience, VA requires the Veteran to hire a property management company.

- Need to make sure land is zoned for multi-unit density

- Builder MUST have experience building multi-unit properties.

One-time vs two-time close vs conventional

| Feature | VA One-Time Close | Two-Time Close | Conventional Construction |

|---|---|---|---|

| Closings | 1 | 2 | 2 |

| Re-qualification | No | Yes | Yes |

| Down payment | 0% (if eligible) | 0–5% (varies) | 5–20% |

| Rate lock | Before construction | Often after construction | Often after construction |

| PMI | No | No | Yes (if applicable) |

| Eligible borrowers | Veterans/eligible borrowers | Veterans/eligible borrowers | All qualified borrowers |

Challenges and considerations

- Limited lender availability: not all lenders offer VA OTC construction

- More documentation: plans, specs, draw schedule, builder package

- Appraisal timing: proposed-construction appraisals can take longer

- Change orders and cost overruns require lender approval and reserves

- Timeline risk: weather, supply, or labor issues can delay completion

Why work with John Thomas

As a VA Construction Loan specialist, I help veterans nationwide understand how to use their benefits to build, not just buy. My team coordinates with experienced builders, manages construction draws and inspections, and helps you close once—on time and without surprises.

Call 302-703-0727 or apply online to see what you qualify for today.

Related programs and resources

- VA Purchase Loan Program — learn more about standard VA purchases

- FHA One-Time Close Construction Loan — compare FHA vs VA construction

- USDA Construction Loan — rural build options

FAQs

Can I use a VA One-Time Close loan to buy land and build?

Yes. You can purchase land at closing or build on land you already own. The land value is included in the appraisal and financing.

Do I need a down payment?

Qualified veterans can finance up to 100% of the land and construction costs plus closing costs if the appraised value supports it.

Can I act as my own builder?

No, you are not allowed to be your own builder. You must hire an experienced builder.

Are manufactured or modular homes eligible?

Yes, if built to HUD/VA standards, placed on a permanent foundation, and approved by the lender.

Do I make payments during construction?

No mortgage payments are required during construction. Mortgage payments start once home is complete and CO has been issued.

What happens if construction goes over budget?

Lenders often require a contingency reserve (for example, 5–10%) for unexpected costs. Change orders must be approved before additional draws are released.

How long does construction take?

Most projects take 6–12 months, depending on weather, materials, permitting, and builder capacity.